Effective Safety Management: The Business Argument

ANDY TILLEARD

EHS Consultant

EazySAFE

Ireland has a good track record for accidents in the workplace. Data shows that Ireland has the lowest standardised incidence rates (per 100,000 employees) of fatal accidents at work for 2018 and averaged rates from 2015 – 2017 at 0.45 and 0.96 respectively.

However, if you were related to any of the people who had been killed at work in these time frames here in Ireland, I’m sure that you would not consider these figures to be of any comfort. Death and serious injury from workplace accidents are avoidable which makes them all the more tragic, especially when we already have the tools in which to effectively manage workplace risk – it’s called effective safety management.

What is effective safety management?

So, the question is what does effective safety management mean and what does it look like? It should be able to deliver a workplace where occupational health and safety risk is managed to a level that is as low as reasonably practicable. This will result in a minimal level or ideally an absence of occupational illness and injury and where such incidents do occur, they are of lower severity and less likely to occur.

Effective safety management also learns from undesirable events when they do happen and mitigates against possible future occurrences. Safety management should be integrated into an organisation’s business or operational management system and considered by top management as an important resource to help the organisation meet its policy objects and not as an add-on to the business.

What is the business case for effective safety management?

If a business is about making money then business owners had better be interested in effective safety management. Accidents are expensive; the more severe they are, the more expensive they become and their impact can be wide-ranging.

Even as far back as 2007, a research report sponsored by the Health and Safety Authority (HSA) in Ireland entitled ‘The costs and effects of workplace accidents – twenty case studies from Ireland’ (1) showed that the “…average cost of the twelve middle-range accidents was approximately €52,000. The costs found were in almost all cases underestimates as productivity losses (with one exception) were not recorded by employers.” (2)

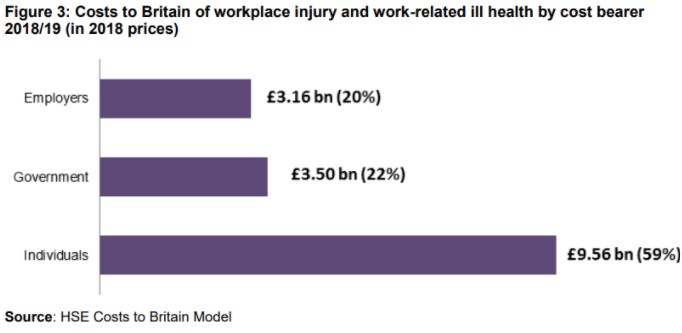

Accidents costs (both direct and indirect) generally apply across three different cost bearers depending upon the severity of the accident; the individual, the company and the government and when examined on a national scale the figures can be astronomical. For example, in the UK figures for 2018/2019 (3) show the following:

This general principle is well understood and of course, there is an almost infinite pool of accident statistics and research which all show the same thing; accidents are expensive, but it is the individual that pays the highest cost in financial and life-changing personal terms.

The business case for effective safety management can also be made by understanding that it is often external forces on an organization that drive or at the very least influence safety behaviours in some organisations because these external factors can limit or restrict how a business operates, gets new customers or investment and therefore impacts on how it operates into the future. Examples include:

- The avoidance of having to pay accident costs which can include increased insurance premiums, workers compensation and legal costs and fines.

- The impact upon an organisations reputation can have potential hidden costs, for example on recruitment where an organisation is not considered to be a responsible or considerate employer within an industry sector.

- The financial resources required to manage safety on a long-term basis are often a fraction of those required to undertake preventative and corrective actions following a serious accident or incident.

- Increasing internal and external stakeholder awareness of how an organisation performs in terms of its safety performance.

- There may be targets or criteria set for company contract bidding processes where safety performance (including metrics such as Lost Time Injury (LTI) rates or Total Recordable Injury Frequency (TRIF)) are used as a part of the tender and assessment process.

- Change is a constant and therefore safety requirements will inevitably become more rigorous and stringent as time passes due to the evolution of safety legislation and societal expectations whether an organisation’s management acknowledges that or not – the bigger the gap between EHS requirements and an organisation’s actual safety management performance, the bigger the hit will be in the event of a serious accident.

- Severe accident events can literally put companies out of business.

Summary

There is really no defense for not being wholly proactive in reducing workplace accidents and incidents, whether that is an SME or a large multinational. Outside of the legal and moral obligations of business owners, it makes financial sense to operate with an effective safety management system as support. Serious accidents and incidents are never blue-sky events and organisations that do not operate with the support of a safety management system are essentially gambling with their employees’ safety coupled with the potential significant financial impact on their business.

Effective safety management does not have to be difficult or complex to initiate or implement – we have been doing it for some time now and the requirements are well defined and easy to understand. There is an old saying that applies here – If you think safety is expensive, try having an accident…

References:

(1) – https://www.hsa.ie/eng/Publications_and_Forms/Publications/Research_Publications/The_costs_and_effects_of_workplace_accidents_-_Twenty_case_studies_from_Ireland.pdf

(2) – Ibid., pVii

(3) – https://www.hse.gov.uk/statistics/pdf/cost-to-britain.pdf

Discover our Safety Training Platform

Train your employees anytime, anywhere with our environmental, health, safety and wellness training platform.

TAILORED TRAINING

Discover our safety training courses and ehs onboardings, which can be customised and offered in several languages.

SAFETY MANAGEMENT

Ensure the distribution of your safety policy by training your permanent, temporary or seasonal staff.

GLOBAL MONITORING

Simplify the management of your safety policy thanks to the numerous dashboards and training reports.